The scientific consensus on the climate crisis is unambiguous, and the economic pathway to address it is increasingly clear: a rapid, unprecedented global transition to a net-zero emissions economy. The debate has thus decisively shifted from “if” to “how,” and more pointedly, to “who pays?” Beneath the grand promises and targets lies a monumental financing challenge—a multi-trillion-dollar annual investment gap that represents the largest peacetime reallocation of capital in history. This is not merely a technical question of moving money, but a profound exercise in intergenerational and intragenerational accounting. The choices we make today about how to fund the climate transition—through public debt, current taxation, or financial innovation—will determine nothing less than the distribution of economic burdens and benefits across generations and continents. We are negotiating the terms of a Great Intergenerational Transfer, and its fairness will define the political viability of the transition itself.

The sheer scale of required investment is staggering. To align with a 1.5°C pathway, global annual clean energy investment alone must triple to over $4 trillion by 2030. This encompasses not only wind farms and solar panels but also the colossal task of modernizing grids, retrofitting buildings, transforming industrial processes, and developing nascent technologies like green hydrogen. Critically, a significant portion of this investment carries the character of public goods: infrastructure that benefits all but which the private sector, left to its own devices, will underprovide due to long payback horizons, high risk, or diffuse returns. The state, therefore, is inevitably cast as the lead risk-taker and coordinator, forcing the central question of public finance: how to mobilize these vast sums without crushing current prosperity or bequeathing an unmanageable debt to the future.

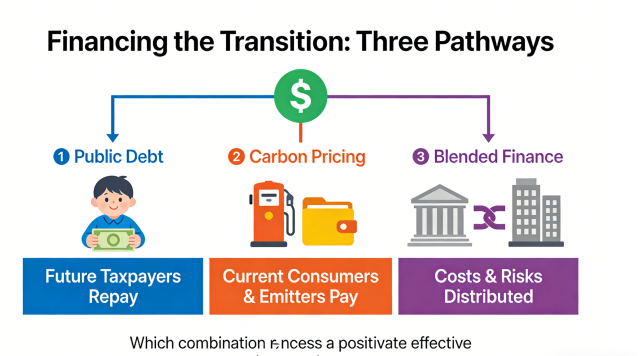

The primary tool in the government arsenal is sovereign debt. Funding the transition through borrowing essentially conducts an intergenerational transfer: it uses the state’s credit to mobilize present-day resources (labor, materials, technology) to build assets that will benefit future generations for decades, while passing the repayment obligation to the taxpayers of tomorrow. This can be a justifiable strategy if two conditions hold. First, if the investments yield a social rate of return higher than the cost of borrowing—by preventing future climate damages, fostering new industries, and enhancing energy security. Second, if future generations are wealthier and better able to bear the repayment burden. This logic underpins calls for expansive “green bonds” and climate-focused fiscal spending. However, with public debt in many advanced economies already at historic highs, this strategy risks perceived fiscal profligacy, potentially crowding out other essential spending or triggering inflationary pressures, placing a dual burden on the young.

The alternative is to finance the transition through current revenue, primarily via carbon pricing (taxes or cap-and-trade systems) and the elimination of fossil fuel subsidies. This approach follows the polluter-pays principle, internalizing the social cost of emissions and generating a revenue stream to fund green investments or compensate vulnerable households. Its intergenerational effect is different: it places the explicit cost on today’s consumers and emitters. While economically efficient, it faces fierce political resistance due to its immediate, visible impact on prices, particularly from lower-income groups and carbon-intensive industries. Its fairness hinges entirely on the recycling of revenues—whether they are used to fund progressive tax cuts, direct dividends, or targeted support for vulnerable workers and regions, or are simply absorbed into general coffers.

Beyond these poles lies a spectrum of blended finance and regulatory mandates. These include green tax credits (a public subsidy through the tax code), risk guarantees to unlock private capital, and requirements on banks, pension funds, and insurers to align their portfolios with climate goals. These mechanisms often obscure the ultimate bearer of cost, distributing it between taxpayers (through forgone revenue), consumers (through slightly higher costs), and shareholders (through adjusted returns). Their intergenerational impact is complex and indirect, but they have become the political compromise of choice, leveraging private capital while softening the immediate fiscal blow.

The calculus of fairness becomes starker when viewed globally. The Global North/South divide represents the most severe intergenerational and international inequity. Advanced economies, responsible for the majority of historical emissions, now possess the deep capital markets, low borrowing costs, and technological edge to finance their own transitions. Many developing nations, bearing minimal historical responsibility but facing extreme climate vulnerability, are saddled with high debt burdens, costly capital, and urgent development needs. For them, the climate transition is not an add-on but an existential threat layered atop a pressing need for energy access, jobs, and growth. Expecting them to finance a transition they did not necessitate, using capital they cannot access affordably, is a profound injustice. The failure of developed nations to meet the $100 billion annual climate finance pledge is more than a broken promise; it is a active blockage of a just transition.

Therefore, the question of “who pays” is inseparable from the questions of “what is paid for” and “who benefits.” A transition financed by debt that only builds large-scale renewable projects for corporate benefit may leave future generations with both debt and a hollowed-out industrial base. A transition financed by regressive carbon taxes without robust compensation may fuel populist backlash and stall progress. A just financial framework must be multi-pronged: it must employ strategic public debt for foundational, high-social-return infrastructure; it must use smart, progressive carbon pricing where politically feasible, with transparent revenue recycling; and it must be underpinned by a major expansion of concessional finance and technology transfer from North to South.

Ultimately, the Great Intergenerational Transfer is a test of our ethical and economic imagination. It asks whether present generations, who have reaped the benefits of fossil-fueled prosperity, will shoulder a meaningful share of the cost to safeguard the future. It asks whether the global community can structure finance not as another form of leverage, but as a vehicle for shared security and opportunity. The climate bill for our past and present consumption is now due. We can choose to pay it in a way that invests in a more prosperous, equitable, and stable future for all who follow, or we can attempt to defer it further, ensuring that the ultimate payment—measured in lives, livelihoods, and shattered ecosystems—will be far more catastrophic and profoundly, unforgivably unfair.

Discuss