In the grand theater of modern capitalism, the initial public offering (IPO) long held a place of singular prestige. It was the crescendo, the moment a company stepped into the luminous arena of public markets, embraced by the scrutiny and capital of the world. This narrative, however, is being quietly rewritten. A profound and structural shift is underway, where an increasing number of mature, high-value enterprises are deliberately bypassing this rite of passage, choosing instead the protracted seclusion of private ownership. This is not a market anomaly but a fundamental reconfiguration of the corporate lifecycle, propelled by a tidal wave of private capital and a growing aversion to the public glare. The consequences—a reshaping of innovation pathways and a narrowing of public wealth participation—signal a quiet revolution in who gets to build, fund, and own the future.

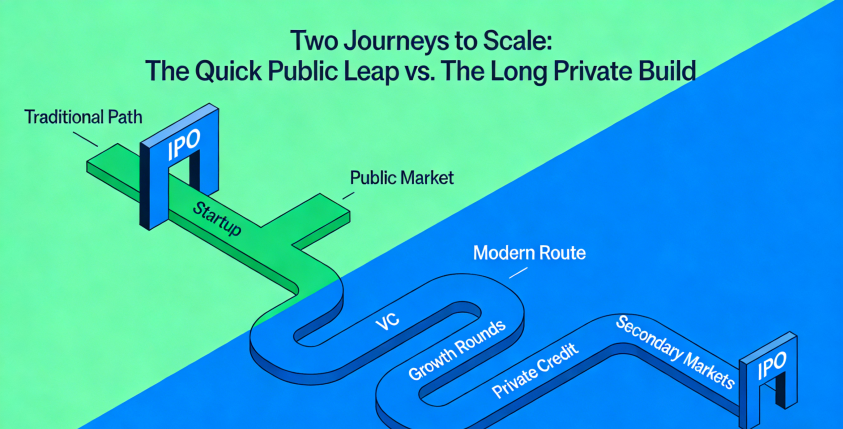

The data paints a stark picture of this retreat. While the IPO pipeline occasionally sputters to life, its character has changed. Today’s public debuts are often smaller, less profitable companies, while the true titans of the new economy amass valuations once reserved for public blue-chips entirely in private hands. The private funding ecosystem has swelled to gargantuan proportions, with global dry powder consistently measured in the trillions. This capital is no longer impatient; it is configured for endurance. As noted in financial analyses, the traditional model of using private investment as a quick bridge to an IPO is being supplanted by a strategy of building enduring, standalone entities in the private sphere. Companies like SpaceX, with its constellation of satellites, or OpenAI, defining the frontiers of artificial intelligence, exemplify this new paradigm. They achieve scale, complexity, and global impact rivaling public corporations, all while their ownership remains concentrated among founders, employees, and a coterie of institutional investors.

The private market’s appeal stems from a powerful dual engine: the magnetic pull of abundant, patient capital and the forceful push away from the burdens of public scrutiny.

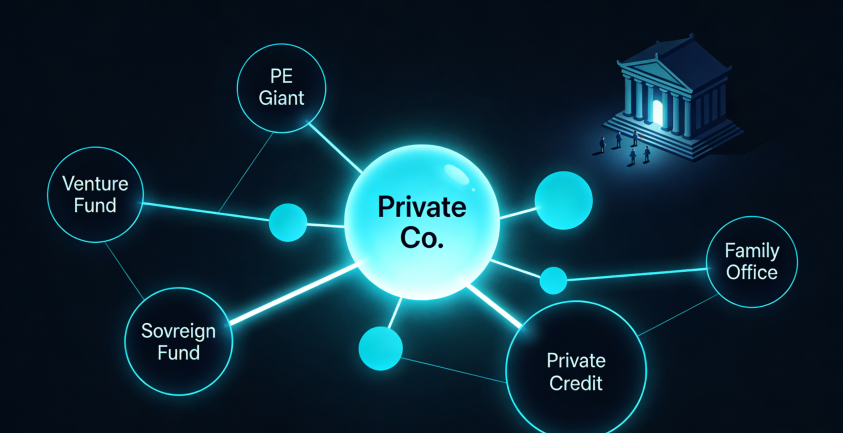

The most significant pull factor is the unprecedented depth and sophistication of the private capital universe. It has evolved far beyond venture capital into a multi-layered financial infrastructure. Growth equity funds, sovereign wealth funds, private credit providers, and crossover investors now form a seamless pipeline capable of funding a company from inception to global dominance. This capital is not only abundant but also aligned with long-term horizons. Freed from the tyranny of quarterly earnings reports, private company executives can pursue strategies that require deep, sustained investment—be it foundational AI research, expensive clinical trials, or building physical infrastructure. This patient capital enables what public markets often punish: the pursuit of outsized, long-term advantage at the expense of short-term profitability.

Simultaneously, the push factors from public markets have grown more intense. Regulatory compliance has become a costly and complex labyrinth, consuming management bandwidth and financial resources better spent on innovation. More fundamentally, public markets are plagued by a pervasive short-termism. Share price volatility, often detached from operational milestones, pressures executives to manage for the next quarter rather than the next decade. This has created a stark valuation disconnect. Private markets frequently reward narrative, total addressable market, and technological moat. Public markets, especially in risk-off environments, revert to stricter metrics of profitability and cash flow. The journey to IPO thus carries the palpable risk of a “down round” in the public eye, a reputational and financial blow that companies and their backers are increasingly unwilling to risk.

The implications of this great migration are profound and multifaceted, reshaping the economic landscape in ways we are only beginning to understand.

- Redefinition of Corporate Adolescence: The very concept of a “mature” company is evolving. A firm can now be global, influential, and decades-old while remaining private. This allows for extraordinary focus and strategic freedom but also consolidates power in fewer, less transparent hands. Corporate governance, once a matter of public debate and regulation, is conducted behind closed doors.

- The Democratic Deficit in Wealth Creation: This shift systematically excludes the retail investor from the primary growth phase of the modern economy’s most dynamic sectors. The most significant value appreciation occurs in the private years, accruing to a limited pool of accredited investors, venture capitalists, and corporate insiders. By the time a company goes public, its most explosive growth may well be in the past. This exacerbates wealth inequality and turns public markets into a secondary arena for asset distribution rather than primary capital formation.

- A New Risk Topography: The risks in the economy are becoming less visible. Systemic risks can accumulate within large, interconnected, but opaque private entities. The performance of these companies, their leverage, and their interrelationships are not subject to daily market tests or public disclosure, potentially creating blind spots for regulators and the broader financial system.

In conclusion, the trend of companies staying private longer is a rational, market-driven response to a changed financial ecology. It is a vote for patience over publicity, for concentration over dispersion, and for strategic latitude over regulatory compliance. While this private market takeover fosters a certain breed of ambitious, long-term innovation, it also erodes the public character of corporate ownership and widens the gap between capital and citizen. The IPO has not vanished, but its role has fundamentally diminished from a necessary destination to a possible, and sometimes inconvenient, turn in a much longer, private road. The age of the permanent private corporation is here, and with it, a quieter, more exclusive model of building the future.

Discuss